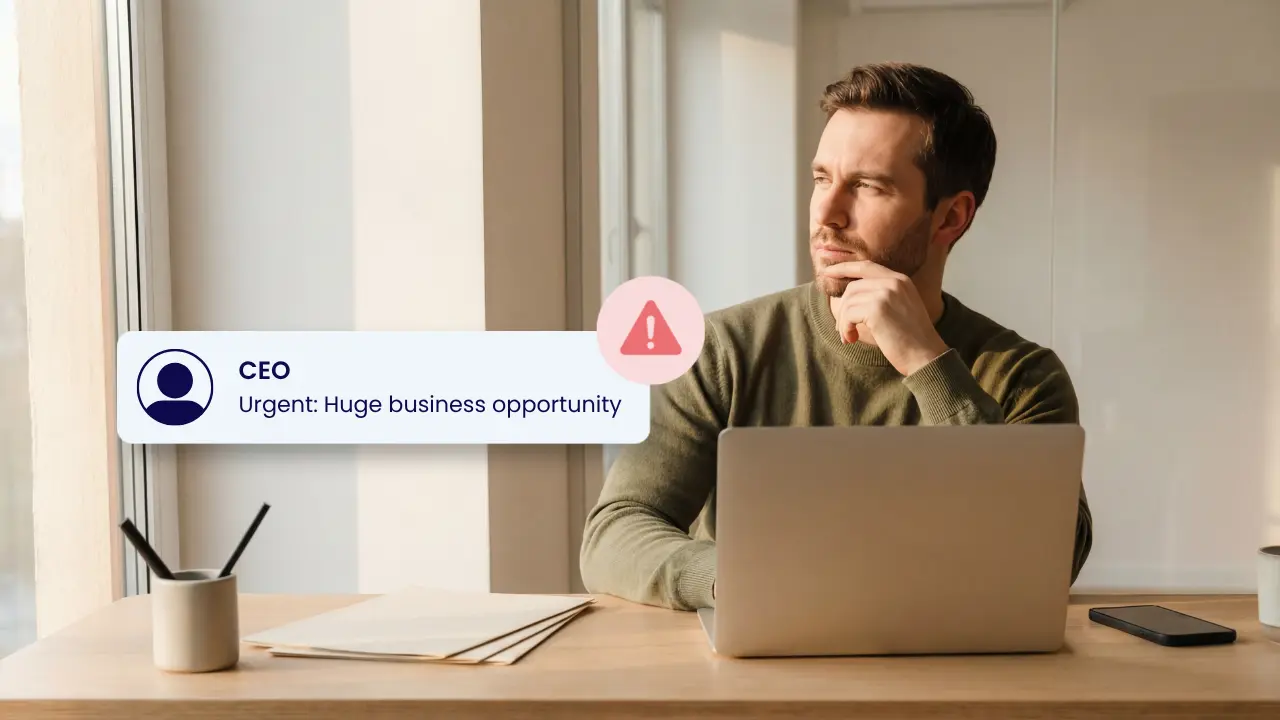

In many organisations, a single message from the CFO can override weeks of process. That is exactly what executive impersonation fraud relies on. The scam is no longer limited to clumsy urgent payment emails.

Finance and AP teams are now dealing with realistic voice cloning, convincing video calls, and messages written to match how your organisation speaks, often arriving at the worst possible time, such as month-end, a system go-live, or during leave.

The aim is simple. Create enough urgency and authority that one person makes an exception, and the controls never get a chance to do their job.

Why are finance teams so exposed to fake CFO pressure

Criminals are usually not trying to break into your ERP first. They are trying to break decision-making. Senior leaders are powerful levers because people are conditioned to respond quickly, and because large payments and exceptions sit closer to finance than most other functions. When the request sounds plausible and time sensitive, it can feel safer to act than to challenge.

What we often see is that the story does not have to be perfect. It only needs to be believable enough to shift the work out of the normal workflow and into a side channel where audit trails are weak, and verification steps become optional.

What does executive impersonation look like in day-to-day AP work?

In practice, this can take the form of CEO fraud in accounts payable, where a payment or approval request appears to come from a senior executive and is used to push AP outside the normal workflow.

Typically, the first move is a surprise request that feels confidential. A staff member is asked to jump on a quick call about a sensitive deal or an urgent supplier situation. A link is shared. On the screen is a familiar face using familiar language.

The next step is the objective: process something outside the standard path, skip the normal approvals, or treat the transaction as an exception because this is coming from the top. Another common pattern is pushing the request into non-standard channels such as SMS, personal email, or consumer messaging apps. That shift matters because it increases the chance the recipient will act before checking, and it reduces the chance the request is captured in a controlled workflow.

The red flags that should trigger a pause and verify

Even as impersonation gets more convincing, certain behaviours remain high risk. When the request uses a new channel, demands secrecy, asks you to bypass workflow, introduces new bank details, or looks out of character for the leader involved, that is enough to slow down.

The point is not to argue about whether it is real. The point is to move verification into a channel you trust and control. In many organisations, the simplest rule holds up best: if the request asks you to break the process, treat it as suspicious, even if it appears to come from a senior person.

When red flags appear, use this simple response process:

Which workflow controls stop executive impersonation fraud before money moves

These controls are designed to reduce the risk of payment fraud by making it harder for urgent, high-pressure requests to bypass approval and verification steps.

The most effective defence is not expecting staff to develop a sixth sense. It is designed so that a convincing impersonation cannot produce an outcome on its own.

First, make non-negotiable rules explicit and enforceable. If a transaction is above a defined threshold, it should only be actioned through the governed workflow. If the instruction arrives outside that workflow, the correct response is to bring it back into the system rather than processing it elsewhere.

Second, use known channel verification for unusual requests. Fraudsters rarely control every channel. A call back to a number from the corporate directory, a fresh meeting invite sent to the corporate address, or a confirmation through your internal platform often breaks the spell because it forces the attacker outside their prepared script.

Third, use segregation of duties that cannot be overridden by urgency or seniority. High-value approvals should require more than one approver, ideally from different roles or reporting lines. That way, the transaction needs more than one brain and more than one point of failure.

Fourth, use risk-based routing so the workflow automatically increases scrutiny when warning signs appear. A high-value invoice with new bank details, unusual timing, or a new supplier relationship should be pushed into a high-risk path without relying on someone remembering to do the right thing.

Bank detail changes deserve an extra rule: verification should be a defined step with evidence, not an informal task completed under pressure. In practice, this is where independent verification adds discipline. Where RapidAP is used, Eftsure can be integrated to verify supplier bank details during change requests, with the outcome recorded and mismatches routed as exceptions rather than handled in side channels.

Finally, culture is part of control design. If people think they will be punished for delaying a payment, they will move fast and hope for the best. If leadership explicitly supports pause, verify, escalate, staff are far more likely to follow the process when it matters.

Key takeaways for stopping executive impersonation

- Treat any request to bypass the normal workflow as a verification trigger, and confirm it through a known channel.

- Make non-negotiable rules enforceable through thresholds and system-only processing, so urgency cannot override controls.

- Separate approvers across roles or reporting lines for high-risk payments, so one person cannot carry the full decision.

- Use risk-based routing so red flags like new bank details, high value, and unusual timing automatically escalate for review.

- Back the process with leadership messaging that protects people who pause, verify, escalate, and record.

Executive impersonation within broader AP governance

Finance and AP teams are increasingly exposed to executive impersonation in AP, including fake CFO payment requests, cloned voices, and urgent side-channel payment instructions.

Executive impersonation is a reminder that fraud is often a workflow problem before it is a technology problem. As part of a broader accounts payable fraud prevention approach, email and chat are useful for notifications, but they are poor systems of record for approvals and high-risk changes. When approvals and exceptions happen inside a governed workflow, it is much harder for an attacker to monetise authority and urgency.

How automation supports fraud controls in AP

Rules-driven workflow tools help by enforcing thresholds, routing work based on risk, and maintaining traceability. The practical value is consistency. Controls do not rely on memory, and exceptions cannot quietly disappear into side channels.

Frequently Asked Questions

Is executive impersonation fraud the same as business email compromise?

Executive impersonation fraud is often treated as part of a broader business email compromise risk, but in practice the key issue for AP is the same: a request appears to come from a trusted senior person and is used to create urgency, secrecy, or an exception to process.

The safest response is not to debate labels, but to verify the request through a known channel and bring it back into the governed workflow before any payment or change is actioned.

What should AP staff do if a senior executive requests an urgent confidential payment?

AP staff should pause, verify, and escalate through a known and trusted channel. If the request asks someone to work outside the normal workflow, skip approvals, or act quickly because of confidentiality or urgency, that alone is enough to treat it as high risk.

The goal is to move the request back into the controlled process, where approvals, audit trails, and verification steps can do their job.

Why are bank detail changes high risk in executive impersonation fraud?

Bank detail changes are high risk because they are one of the fastest ways for a convincing impersonation to turn into a payment loss. When a request includes new account details, unusual timing, or pressure to act quickly, verification should be a defined control with evidence, not an informal task completed under pressure. Independent verification helps prevent these requests from being approved through side channels or assumptions.

Can AP automation prevent executive impersonation fraud on its own?

No. Automation supports fraud control, but it does not solve fraud by itself. Its value is in enforcing thresholds, routing unusual requests into higher-risk workflows, maintaining traceability, and reducing reliance on memory or manual judgement under pressure.

The strongest defence still comes from combining workflow rules, known-channel verification, segregation of duties, and leadership support for staff who pause and verify.