For most finance leaders, the question is not whether AP automation is a good idea in principle. It is whether the investment still makes sense once implementation effort, process change, approval behaviour and the messy reality of exceptions are taken into account.

The most common mistake in an AP automation ROI model is focusing only on data entry savings. Data entry is visible, but it is rarely the biggest driver of cost or risk. What usually consumes time across the business is chasing approvals, resolving exceptions, handling supplier enquiries, cleaning up accruals and retrieving audit evidence.

A defensible investment case balances three things: efficiency, control and financial visibility.

In practice, AP automation is usually worth the investment when invoice volume, approval delays, supplier enquiries, rework or audit evidence retrieval create measurable cost and control issues. The strongest return usually comes from reducing rework, improving governance and giving finance teams better visibility across the invoice lifecycle.

What does AP automation ROI measure

AP automation ROI measures the value gained from improving the accounts payable process compared with the cost of implementing and operating automation. In practice, accounts payable automation ROI should reflect both direct processing savings and wider improvements in control, visibility and exception management.

That value may include reduced manual handling, fewer approval delays, lower exception volumes, fewer supplier enquiries, stronger audit evidence and better invoice visibility.

In many organisations, the return is spread across finance, operations, procurement and budget owners. An invoice may be received by AP, queried by a supplier, followed up by a manager, corrected by finance and reviewed again during month-end or audit. Each touchpoint adds cost, even if it does not appear as a separate AP task.

A useful ROI model should answer three practical questions:

- Where is time being spent?

- Where are errors being repeated?

- Where does the organisation lose visibility or control?

This is where AP automation ROI becomes more than a cost-saving exercise. It becomes a way to assess whether the current process is sustainable.

How to calculate the ROI of AP automation

A practical calculation starts with the current cost and effort required to process invoices manually.

A simple way to frame the calculation is:

Start by measuring current invoice volumes, average handling time, exception rates, approval delays, supplier enquiry volumes and audit retrieval effort. Then estimate how much of that work can reasonably be reduced through automation.

Measurable benefits may include:

- Lower invoice processing effort

- Fewer manual corrections

- Reduced supplier follow-up

- Less time spent chasing approvals

- Faster invoice status visibility

- Reduced duplicate payment risk

- Less effort preparing for audit or month-end

Costs should include software, implementation, ERP integration, internal project time, training, supplier communication and ongoing administration.

A conservative ROI model is usually more credible than one that assumes every invoice will move through the process without exception.

AP automation benefits that create measurable return

The strongest AP automation benefits are usually practical and observable.

Reduced manual handling

Manual invoice handling creates effort at every stage, from capture and coding through to approvals, exceptions and filing. Automation can reduce repetitive work by capturing invoice information, applying configured rules and routing invoices to the right people.

Faster approval cycles

Delayed approvals can affect supplier relationships, payment planning and month-end visibility. Automated workflows help make invoice status clearer and reduce the need for AP teams to chase approvers manually.

This does not remove the need for business accountability. It makes approval ownership more visible.

Better exception management

Exceptions are often where AP teams lose the most time. Missing information, purchase order mismatches, incorrect coding and approval uncertainty can all slow the process.

A structured workflow helps exceptions move to the right person instead of sitting in inboxes or being handled through informal follow-up.

Stronger audit evidence

A clear record of invoice actions, approvals, notes and supporting documents can reduce the effort required during audit or internal review.

For CFOs and finance leaders, this benefit is important because it supports control and accountability, not just speed.

ROI claims to treat carefully

Some AP automation claims should be reviewed carefully before they are included in an investment case.

The first is touchless processing. A high touchless rate can be useful, but it should not be the main measure of success. In practice, invoices still need controls, matching rules, exception handling and approval logic. Touchless processing only creates value when the underlying process is reliable.

The second is immediate headcount reduction. Many organisations do not reduce AP headcount after automation. Instead, they redirect staff towards supplier management, exception reduction, reporting, governance and process improvement.

That can still be a strong return, but it should be described honestly. The benefit is often capacity release, not direct labour removal.

The third is instant ROI. Benefits usually improve over time as supplier behaviour, approval discipline and exception handling mature.

AP Automation costs that are often underestimated

Finance teams often underestimate the internal effort required to make automation work properly.

Process alignment

Delegation of authority, approval pathways, coding rules, purchase order matching rules and exception ownership need to be agreed before automation can operate consistently.

ERP integration

Data must move cleanly between systems, and the team needs to understand how failed exports, validation errors and master data issues will be managed.

Change management

Approvers need clear expectations. AP teams need training. Suppliers may need updated invoice submission instructions. Without this, the organisation can end up running old and new processes at the same time.

Ongoing ownership

Workflow rules, approval limits and user roles change as the business changes. Someone needs to own that maintenance.

For a broader view of how automation fits into finance operations, see the Efficiency Leaders guide to accounts payable automation.

When AP automation may not deliver ROI

AP automation may not deliver strong ROI when invoice volumes are low, the existing ERP workflow is already mature, or the organisation has very simple approval requirements.

It can also underperform when the business is unwilling to change the behaviours that cause AP delays. For example, automation will not fully solve poor purchase order discipline, slow receipting, unclear approval ownership or inconsistent supplier instructions.

In these cases, the business may still proceed for control, auditability or scalability reasons. However, the ROI case should be framed around those outcomes rather than simple processing cost reduction.

What vendors should prove before you invest

A vendor should be able to show how the solution handles real AP complexity, not just a clean invoice demo.

Ask how the workflow manages missing information, duplicate invoices, purchase order mismatches, approval delays, leave coverage and escalation. Ask how invoice data is validated before it reaches the ERP. Ask what happens when an export fails.

It is also worth asking how reporting works. Finance teams need visibility across invoice status, ageing, approval bottlenecks and exception volumes. Without this, automation may reduce some manual work but still leave leaders without reliable process insight.

For related reading, see the Efficiency Leaders article on automating accounts payable.

How rules-driven AP automation supports investment value

AP automation ROI depends on process control as much as processing speed.

Rules-driven AP automation helps by applying defined validation rules, routing invoices through configured workflows and making exceptions visible. This gives finance teams a more consistent way to manage invoice capture, approvals, exception handling and ERP export.

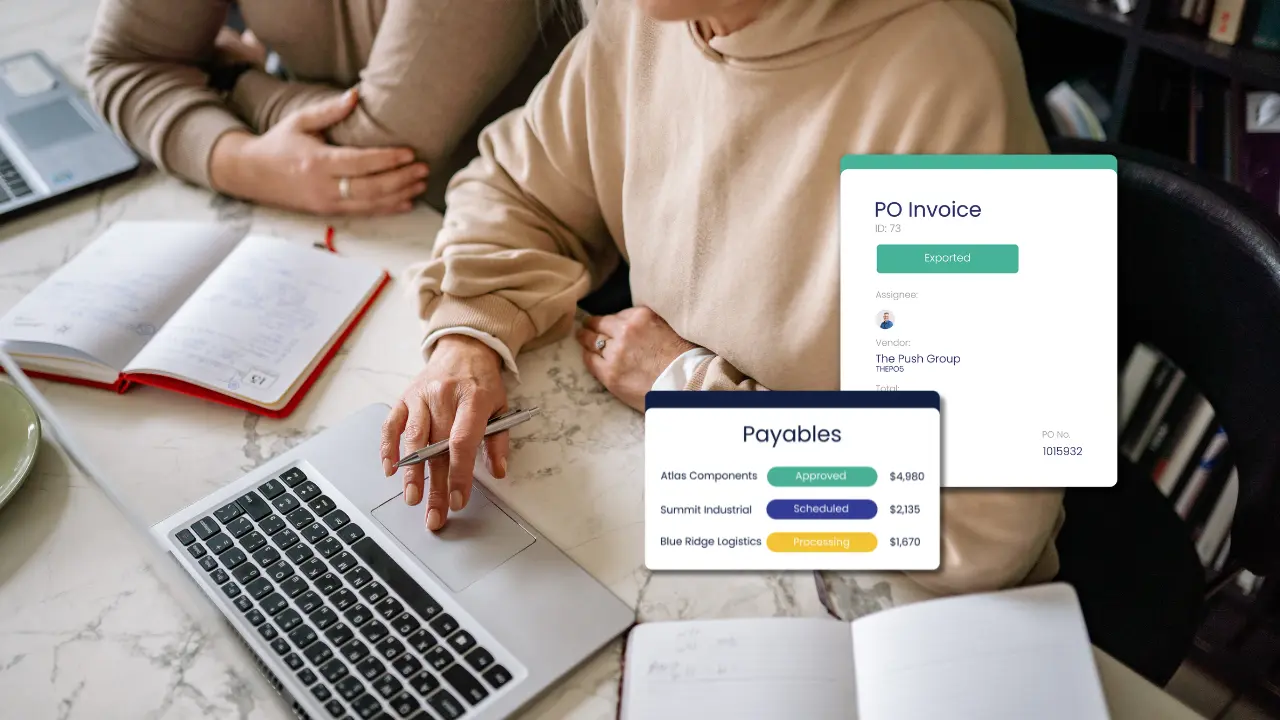

Efficiency Leaders’ RapidAP supports invoice and credit note capture, approval workflows, exception routing, invoice lifecycle visibility, searchable invoice records, audit trails and ERP export. It is designed to support governance-focused invoice processing through configured rules and defined workflows.

Key takeaways

- AP automation ROI should be based on measurable process improvement, not broad automation claims.

- The strongest returns usually come from reduced rework, faster approval visibility, better exception handling, stronger audit evidence and improved month-end control.

- Finance teams should include implementation effort, ERP integration, change management and ongoing workflow ownership in the investment case.

- AP automation is most likely to be worth the investment when manual invoice handling creates repeated cost, delay or governance risk.

- A credible ROI model should be conservative, practical and based on how invoices move through the organisation today.

Frequently Asked Questions

What is a good AP automation ROI?

A good AP automation ROI is one that can be supported by measurable reductions in manual effort, rework, approval delays, supplier enquiries or audit preparation time. The best ROI models are conservative and based on current process data.

How do you calculate accounts payable automation ROI?

Calculate the annual measurable benefit of automation, subtract the annual cost, then compare the result against total investment. Include software, implementation, ERP integration, internal effort, training and ongoing administration.

When is AP automation worth the investment?

AP automation is usually worth the investment when invoice volumes, approval delays, exception handling, supplier follow-up or audit requirements create material cost and control issues.

When might AP automation not be worth it?

AP automation may not be worth it when invoice volumes are low, processes are already well controlled, or the organisation is not prepared to change approval, receipting or exception management behaviours.